Tensions in an Accelerating World

Global survey on financial, political and social issues reveals future-shaping divides

If you feel like the pace of life is speeding up, that news, information and new technologies are moving faster and faster, you’re not alone.

The international advisory firm for which I work, the Brunswick Group, just released a global survey of more than 40,000 people from 26 markets gauging sentiments on financial, political and social issues. Throughout the world, we found, people see the rate of change accelerating, creating new tensions and animating old ones.

As just one example of this acceleration, consider the National Intelligence Council’s study of the length of time between a technology’s invention and its distribution to 25 percent of the U.S. population. It took 46 years for electricity to reach a quarter of the country. The telephone took 35 years. The radio took 31. Color TV took only 18 years, mobile phones 13 years, and the internet only seven years from commercial inception to adoption by 25 percent of the country.

We live in a world dominated by the technologies only science fiction writers foretold: Dick Tracy-style two-way wrist TVs, talking computers, weaponized lasers, cyberwarfare, cryptocurrencies, virtual reality and robots. It’s little surprise then that our global research among 42,965 citizens speaking 25 languages found large majorities operating in a technological fast-forward. In North America, 72 percent of respondents reported that the pace of technological change was moving “quickly.” In just the U.S., this number was 83 percent! By comparison, 67 percent of Europeans and 70 percent of Asians report technology changing quickly in their country. Everyone is feeling technological acceleration.

And, not only are the people of the world feeling this acceleration, they are expecting it. At least half of the people living in both emerging and developed markets expect telecommunications, automobiles and energy to change “a lot” over the next 20 years. They are expecting technological revolution in the energy they use, their mobility and their communications. Talk about a changing world! And with such change comes conflict.

Creative Destruction

Our global perception research identified three significant tension points:

Hope versus Fear

Independence versus Interdependence

Man versus Machine

These three tensions are especially critical for Mensans to understand because in many venues Mensans are driving the accelerating change around us, leading organizations and communities through this turbulent period of creative destruction.

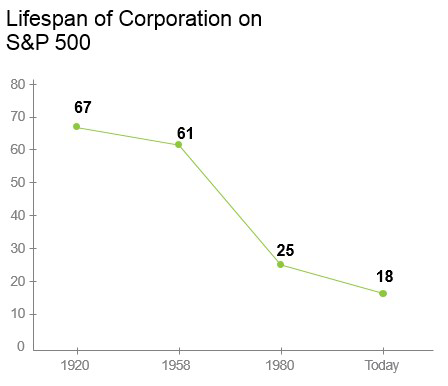

To illustrate one aspect of this creative destruction, Richard Foster at Yale University studied the average “lifespan” of a corporation on the S&P 500. In 1920 that lifespan was an average of 67 years. By 1958, the corporate lifespan had dropped to 61 years. By 1980, the advent of the information age, the average S&P lifespan was 25 years. By 2012, the average corporate lifespan for concerns on the S&P 500 was only 18 years.

Not surprisingly then, people across the planet are expecting creative destruction of their employers. In our global research, 16 percent of employees in emerging markets and 22 percent of employees in developed markets reported that it was “unlikely” that their employer “will exist in a similar form” in 20 years.

Interestingly, of all the people on the planet, Japanese employees expected the most creative destruction, with one-third saying that their employer is unlikely to exist in a similar form in 20 years. Japan, a high-tech leader, has the greatest expectation of technological disruption and reinvention.

Racing the Telegraph

Japan brings us to a cautionary tale about the models we use to think about the world. After 220 years of isolation from the West and limited technological advancement, Commodore Matthew Perry helped to reopen Japan’s Tokugawa shogunate. In 1854, Perry finalized diplomatic ties and presented the Japanese with many gifts, including a miniaturized steam-powered locomotive and the Victorian internet — the telegraph. To test this new technology, Japanese dignitaries and bystanders would wait for hours in order to see the telegraph operators at work. Many would race against the telegraph, running alongside the telegraph wire in a futile attempt to outpace the telegraph message. As Perry wrote in his account of these events, “Day after day the dignitaries and many of the people would gather, and, eagerly beseeching the operators to work the telegraph, watch with unabated interest the sending and receiving of messages.”

The Japanese witnesses simply could not believe that the telegraph could send messages quickly and over a vast distance. Like most people before the invention of the telegraph, they implicitly equated communications with transportation. With the notable exception of the African “talking drums” and military flag corps, communication was transportation. But the telegraph shattered that link, and distance has been dying ever since. These Japanese dignitaries and bystanders had an outdated model of communication and had to relearn.

We are now those dignitaries and bystanders. We have models of the world that we have learned through observation, anecdote and our peers. And when accelerating change makes these models obsolete, we resist and scramble for new understanding.

The acceleration of technology, information and life has us all scrambling for new understanding. And the world is grappling with the resulting tensions.

Flags, Markets or Mayors

Today we tend to use flags or markets as the units of analysis for different parts of the world. That is, we think about the world in terms of nation states (flags) or markets, developed versus emerging.

But our research suggests that we should also think about the world in terms of cities, specifically megacities. Think London, New York, Sao Paulo, Tokyo, Beijing, Hong Kong, Jakarta, Mexico City, etc. Across the globe, megacity residents appeared to have more in common with each other than with their own countrymen in smaller cities and towns.

As just one example, we asked citizens around the world to rate their own personal financial situation compared to most other people “your own age in your country.” By a net 26 points, megacity residents said they were doing better than people their age in their country, with 47 percent saying they were better off and only 21 percent saying they were worse off. But outside of megacities the answer was essentially a tie, with 33 percent saying they were better off and 28 percent saying they were worse off.

Megacities are the beating heart of a globalized economy. And the gap between megacities and everyone else is a core trend today. London residents had a diametrically different view of Brexit than their fellow citizens outside London. In the recent U.S. presidential election there was a well-documented gulf between Democratic voters in large, coastal cities and Donald Trump voters in the heartland. This same trend is well reported in China, where coastal megacities have prospered dramatically relative to the Chinese interior.

A New Model

We are all familiar with the Three-World Model, proposed by French demographer Alfred Sauvy in 1952: the first world as the large, capitalist nations; the second world as the communist nations; and the third world as non-aligned, post-colonial nations in Latin America, Africa and Asia. This model is based on the nation as the unit of analysis.

In the 21st century, we should consider a three-networks model based on cities, with the first network composed of laterally integrated megacities bound by air travel and data flows, the second network composed of national cities strongly tied to their national economies, and the third network composed of small towns and rural areas tied to their regional economies.

Our global research supports this new model. And it’s through this lens that we can better appreciate the global tensions created by a fast-changing world.

Hope Versus Fear

There is a popular belief in the West that we live in an age of rage — of anger and of pessimism. This may be true in some parts of the West, but it is not true globally. In fact, our research finds large differences in optimism and pessimism. For example, citizens of the United Arab Emirates, Switzerland, China, India, Singapore, Sweden, Indonesia, Denmark, Australia, Finland, Germany, Austria, Thailand and the U.K. showed net positives when asked how things were going in their country. Citizens of Italy, Brazil, France, Spain, South Africa, Mexico, Poland, Japan, Belgium and the United States were net negative in their perceptions of their country’s current well-being. Italy, Brazil and France were the most pessimistic, suggesting that the economic situation of a country weighs heavily on its views.

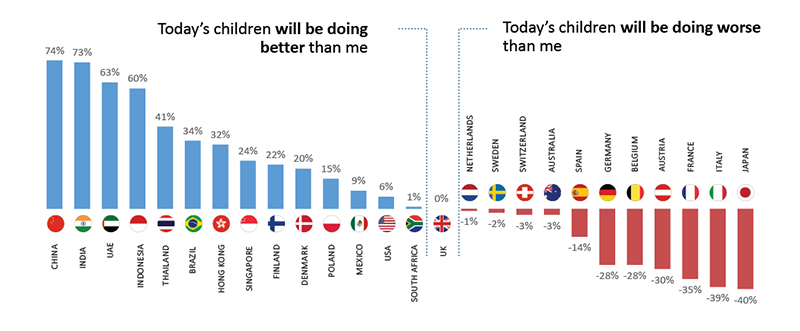

But hope is about the future. And when social researchers ask about the future, they ask about expectations for children. Will our children be better off than we are today? When asked about their children’s future, people in emerging markets were dramatically more optimistic than those in developed markets. In fact, while emerging markets were a net +40 in optimism about their children’s future, developed markets were pessimistic about their children’s future, a net -9 points. To highlight this further, the nations most optimistic that their children will have a better future are China, India, the UAE, Indonesia, Thailand and Brazil. The nations most pessimistic about their children’s future are Japan, Italy and France.

This pessimism in the developed West has enormous political implications. If we continue to observe these levels of pessimism and angst over the future, we can rationally expect a radicalization of politics in developed markets, including populist-nationalist movements.

When we move beyond a nation-state analysis and look at megacities, a different pattern emerges, with megacity residents a net +35 points optimistic about their children’s future, and those in small cities and towns with a much less optimistic view, a net +2 points. Hidden underneath this is the fact that residents of smaller cities and towns in developed markets are a net -13 points pessimistic about their children’s future while their developed market countrymen in megacities are a net +13 points optimistic about their children’s future. These findings help explain Brexit and the recent U.S. presidential election, in which large and coastal regions voted one way and rural and interior regions voted another.

Could megacity mayors band together and represent their collective interests? Could megacity mayors coordinate policies and become a world change agent in their own right? It’s one potential future.

Independence versus Interdependence

Independence versus interdependence, the tension between nationalistic self-reliance and transnational cooperation, has been a consistent theme over the past several years. Brexit and the rise of economic nationalism in the West, especially the U.K., U.S. and France, are related events and driven by negative social reactions to some elements of globalization.

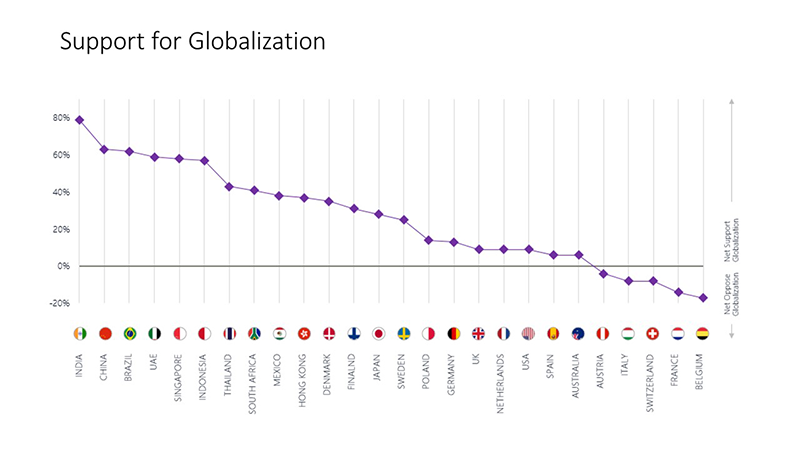

Our research found that while globalization is extremely popular in emerging markets (60 percent positive, 10 percent negative), globalization is much less popular in developed markets (36 percent positive, 23 percent negative). To illustrate this, net support for globalization was +79 points in India, +63 in China and +62 in Brazil but net negative in Austria (-4), Italy (-8), Switzerland (-8), France (-14) and Belgium (-17). (The U.S. and the U.K. were both +9.)

This explains why economic nationalists have risen in the West, why the Trump administration is so focused on rewriting international trade deals and why Chinese President Xi Jinping ardently defended globalization in January at the World Economic Forum in Davos.

There are three key components of globalization — idea exchange, product exchange and labor exchange. The first is popular in both developed and emerging markets. The second is popular in emerging markets and somewhat popular in developed markets (with the exception of offshoring and foreign acquisition of domestic businesses) and very popular in emerging markets. And labor exchange is much less popular generally and very unpopular in developed markets.

Taken together, this explains the trend in many developed nations toward tighter immigration enforcement, the unpopularity of trade deals such as the Transatlantic Trade and Investment Partnership and political campaigning for trade protectionism.

The problem is that these trade protectionist trends are out of step with the 21st century trade in two basic ways. The first is that an increasing share of commerce is in digital, information and entertainment products transacted online. In fact, McKinsey Global Institute research has found that “soaring flows of data and information now generate more economic value than the global goods trade.” The second is that industrial automation via robotics is likely to reduce the importance of global wage rate differences, which would result in the re-localization of manufacturing. Why manufacture a product with robots overseas (incurring the resulting shipping costs) when you can manufacture a product with robots at home?

Man Versus Machine

The rise of robots and algorithms brings us to the third global tension, workforce automation.

A 2013 Oxford University study found that roughly 47 percent of current jobs were “at risk” of automation in the next 20 years. After studying 702 occupation categories, the research team applied an automation score to each job. The most automatable jobs included telemarketers, title examiners, insurance underwriters, tax preparers, insurance claims clerks, brokerage clerks, loan officers and milling and planing machine operators — all jobs where artificial intelligence or industrial robots could eventually be able to do the work.

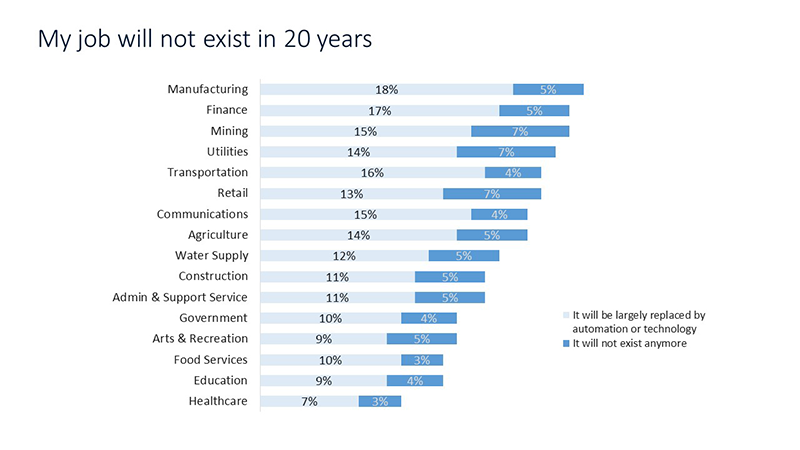

Our global research finds that, contrary to popular belief, many employees clearly see an automation tsunami on the horizon. In fact, 19 percent of employees in developed markets believe it is unlikely that “the type of job” they do now will “exist in a similar form” in 20 years. Among baby boomers in developed markets, this number is a whopping 28 percent! Manufacturing employees were, unsurprisingly, the most likely to believe that their jobs would be automated, but the sectors with the second-highest expectation for automation may surprise you — financial services and mining.

Globally, 23 percent of manufacturing employees believe their jobs will be “largely replaced by automation or technology” or “not exist anymore.” This is entirely rational based on the dramatic increase of industrial robots. And while manufacturing employees were the most likely to see automation on their horizon, 22 percent of financial services and mining employees anticipated what economists call “technological unemployment.” Workers in transportation and storage (20 percent) and workers in wholesale and retail trade (20 percent) also reported higher expectations of automation.

Automation skeptics believe that the rate of automation is being overestimated and that the adoption rate will be slower. Automation alarmists, on the other hand, are very concerned about a future dystopia in which a large underclass is unemployable. They tend to support policies like universal basic income as one solution. Automation specifists see a much more complex future in which some tasks are rapidly automated and many others are not. This group tends to support large, national training and reskilling efforts. Automation humanists envision a much better world in which humans can focus on work that only humans do best, such as social and creative enterprises. This group tends to focus heavily on the end of drudgery.

Whatever your position, the tension between man and machine will clearly race forward. MIT economists Andrew McAfee and Erik Brynjolfsson argue that the solution is a synthesis, not a race against the machine but a race with the machine. If that is the case, then we are likely to see the creation of significant workforce training and upskilling programs.

The Future We Make

Our global research identified some large tensions and significant challenges. A dispassionate analysis of this global perception data presents many sobering potential futures. The famous futurist Jim Dator hypothesized that there are four basic archetypes that humans use to think about the future: continuation, collapse, the disciplined society and transformation.

Continuation represents the perpetuation of the trends outlined here: decline of the West, rise of trade protectionism, severe economic dislocation from technological unemployment and great expectations in emerging markets destroyed by sluggish growth on an aging planet. Collapse means a dystopian future in which the global system and post-war prosperity evaporate. The disciplined society is a future in which we crash against limits and refocus culture and institutions around a core belief or purpose as a means of conserving resources. And transformation would be the creation of an entirely new world based on cascading technological breakthroughs and the system created to harness them.

It is easy to review the insights from our global research and imagine continuation, collapse or the disciplined society. It is much harder to imagine and work for a transformational future. We need to identify and support transformational thinking from the edges, from unlikely corners. And we need to solve 21st century problems with 21st century thinking, as well as the insights of Generation Z, our first truly digital and AI natives.

We could look at this data, at our current state, and predict painful upheaval mixed with steady decline. But the best way to predict the future is to make it.